A Nation on the Brink: March 1933

When Franklin D. Roosevelt took the oath of office on March 4, 1933, roughly 4,000 American banks had already failed since the stock market crash of October 1929. Citizens were hoarding gold coins, draining reserves from struggling institutions at an alarming pace. Within 36 hours of his inauguration, Roosevelt declared a national bank holiday under the authority of the Trading with the Enemy Act of 1917, halting all banking transactions across the country. Congress convened in emergency session on March 9, and by 8:30 that evening, the Emergency Banking Relief Act had passed both chambers and received Roosevelt’s signature. In terms of sheer legislative velocity, it remains one of the most remarkable events in American financial history, and its direct consequences are written into every piece of paper money printed after the spring of 1933.

What the Act Actually Did: The Key Provisions

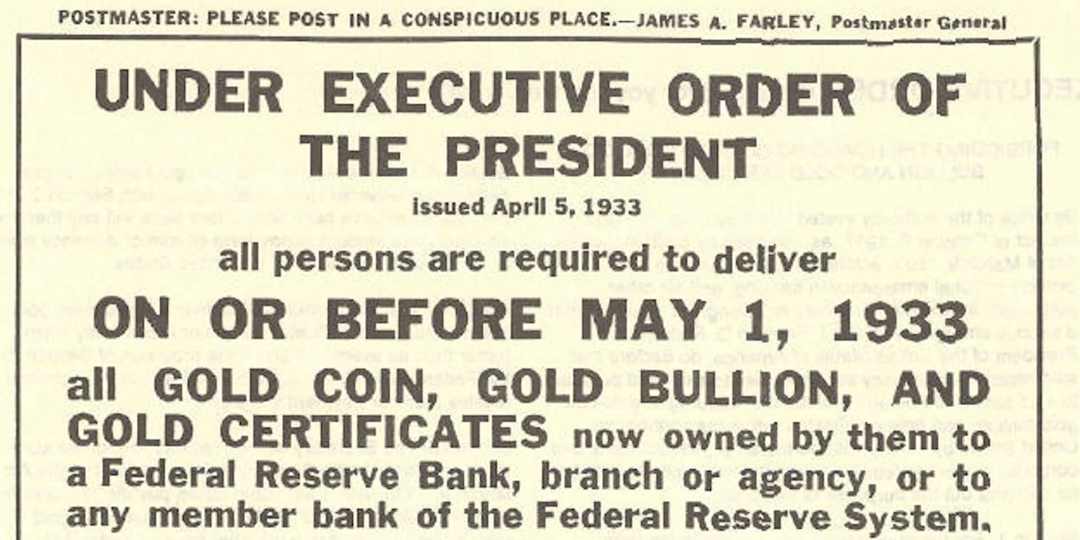

Most popular accounts of the Emergency Banking Relief Act focus on the reopening of solvent banks and the creation of a federal inspection framework. Those provisions matter enormously to economic historians, but for currency collectors the critical section is Title IV. That section amended the Federal Reserve Act to allow Federal Reserve Banks to issue Federal Reserve Notes backed by any sound assets they held, not merely the gold and commercial paper that had previously served as collateral requirements. In plain language, it severed the mandatory gold backing requirement for new Federal Reserve Note issuances and set the stage for Executive Order 6102 on April 5, 1933, which prohibited private gold hoarding, and then for the Gold Reserve Act of January 30, 1934, which officially devalued the dollar from $20.67 to $35.00 per troy ounce.

The practical effect on circulating currency was profound. Federal Reserve Notes issued under the Series 1928 and Series 1928-A dates still carried the obligation: “Redeemable in gold on demand at the United States Treasury, or in gold or lawful money at any Federal Reserve Bank.” The Series 1928-B notes, which began entering circulation around 1933 and 1934, transitioned to a revised obligation. By the Series 1934 dated notes, that gold-payable promise had been stripped away entirely, replaced with the simpler: “This note is legal tender for all debts, public and private, and is redeemable in lawful money at the United States Treasury, or at any Federal Reserve Bank.” Even that language was eventually shortened in later series to just the legal tender clause.

When examining pre-1934 Federal Reserve Notes, look at the obligation text beneath the portrait. The phrase “Redeemable in gold on demand” is your clearest visual confirmation that a note predates the Act’s full implementation. Notes bearing this language in high grades command significant premiums precisely because they represent the last tangible artifact of the gold standard era in circulating paper money.

Series 1928 and the Gold-Payable Obligation: What Collectors Should Know

The small-size Federal Reserve Note design was introduced in 1929 with the Series 1928 date. These notes, printed in denominations from $5 through $10,000, prominently stated their gold redeemability. The Series 1928 notes bore signatures of Treasury Secretary Andrew W. Mellon and Treasurer of the United States Walter O. Woods, while the Series 1928-A notes paired Ogden L. Mills with Woods. The Series 1928-B notes, with signatures of William H. Woodin and Woods, were where the transition truly began, and some collectors refer to this as the “bridge series” because notes with this date were printed both before and during the legal transition period.

The distinction between gold-obligation and non-gold-obligation notes within the 1928-B series is subtle but real. The Bureau of Engraving and Printing did not immediately overhaul every plate after March 9, 1933. The obligation language change was implemented progressively through 1933 and into early 1934 as new printing plates were prepared. Collectors who specialize in this transition period often seek out block letter progressions and Federal Reserve district combinations to map exactly when each district shifted its plate text.

High-denomination gold-clause Federal Reserve Notes from 1928 and 1928-A, particularly $500 and $1,000 notes, are among the most sought-after items in all of small-size currency collecting. Even circulated examples in grades of VF-25 or EF-40 can bring four to five figures at auction. Focus on clean, unrepaired examples since pressed or washed notes are common in this area due to their high face value relative to the era.

Gold Certificates: A Parallel Story

The Emergency Banking Relief Act and Executive Order 6102 did not just affect Federal Reserve Notes. Gold Certificates, which had circulated alongside Federal Reserve Notes since the introduction of the small-size series, were formally called in by the government in 1933. Holders were required to exchange their Gold Certificates for Federal Reserve Notes at par. The Series 1928 Gold Certificates, bearing the distinctive bright yellow-gold reverse and the obligation “This certifies that there have been deposited in the Treasury of the United States X dollars in gold coin payable to the bearer on demand,” became legally non-circulating almost overnight.

Technically, Gold Certificates remained legal tender through the Gold Reserve Act of 1934, but private ownership was restricted. Today, Series 1928 Gold Certificates in denominations from $10 through $100 are legal to own and actively collected. The $100,000 Gold Certificate (Series 1934, bearing Woodrow Wilson’s portrait) was never intended for public circulation and was used only for interbank transfers; it is illegal for private collectors to hold, though the notes are well documented in institutional collections.

Silver Certificates and United States Notes: The Surviving Alternatives

The legislative upheaval of 1933 had an interesting side effect on Silver Certificates and United States Notes. Because neither currency type carried a gold obligation, both survived the transition without requiring major plate alterations. Silver Certificates continued to promise silver coin or silver bullion redemption well into the 1960s (the silver redemption privilege was ended for Silver Certificates in June 1968 by Public Law 90-29). United States Notes, the direct descendants of the Civil War greenbacks, carried no commodity redemption promise at all and simply stated their legal tender status. For collectors, this means that Series 1928 United States Notes (the Red Seal $2 and $5 denominations) look and read almost identically to later series, unlike their Federal Reserve Note counterparts where the obligation text changed dramatically.

If you are building a type set that illustrates the 1933 monetary transition, consider pairing a Series 1928 Federal Reserve Note with gold-clause language alongside a Series 1934 Federal Reserve Note of the same denomination and district. The contrast in obligation text is immediately visible under magnification and makes for a compelling display in a currency album with narrative labels explaining the legal change.

The Series 1934 Federal Reserve Notes: First Children of the New Order

With signatures of Henry Morgenthau Jr. (Treasury Secretary from January 1934) and Treasurer William A. Julian, the Series 1934 Federal Reserve Notes represent the first fully post-gold-standard small-size currency. The obligation text now read: “This note is legal tender for all debts, public and private, and is redeemable in lawful money at the United States Treasury, or at any Federal Reserve Bank.” Crucially, the word “gold” appeared nowhere in that promise.

The Series 1934 notes were produced in substantial quantities across all twelve Federal Reserve districts for denominations from $5 through $10,000. High-denomination Series 1934 notes, particularly the $500 (McKinley portrait), $1,000 (Cleveland portrait), $5,000 (Madison portrait), and $10,000 (Chase portrait) examples, circulated primarily among banks and were recalled in 1969 under a Federal Reserve Board policy that discontinued high-denomination notes. Surviving examples command extraordinary premiums today, with even worn $1,000 notes regularly achieving four-figure prices.

| Series / Date | Type and Denomination | Approx. Surviving Population | Rarity |

|---|---|---|---|

| 1928 | Federal Reserve Note $5 (gold clause, all districts) | Tens of thousands across districts | Common |

| 1928-A | Federal Reserve Note $100 (gold clause) | Several hundred per district (grade-dependent) | Scarce |

| 1928 | Federal Reserve Note $500 (gold clause) | Fewer than 100 known fine or better | Rare |

| 1928 | Federal Reserve Note $1,000 (gold clause) | Under 200 across all districts | Rare |

| 1928 | Gold Certificate $20 | Moderately available in circulated grades | Scarce |

| 1928 | Gold Certificate $100 | Scarce in EF or better | Scarce |

| 1928-B | Federal Reserve Note $100 (transition obligation) | Variable by district; Boston and Minneapolis scarcer | Scarce |

| 1934 | Federal Reserve Note $5,000 (first post-gold series) | Fewer than 150 known nationwide | Key Date |

| 1934 | Federal Reserve Note $10,000 | Approximately 336 known, mostly in institutional hands | Key Date |

| 1934 | Federal Reserve Note $1,000 (Atlanta district) | Among lowest surviving populations by district | Rare |

Legacy on the Collecting Market

The Emergency Banking Relief Act created what numismatists now recognize as the single most important type boundary in small-size United States currency. The difference between a note that promises gold and a note that does not is not merely historical curiosity; it reflects a fundamental redefinition of what money legally is in the United States. Collectors who focus on the 1928 through 1934 transition period are essentially documenting the moment the country moved from commodity-backed currency to pure fiat money, a shift whose reverberations are still debated by economists and monetary historians today.

From a purely practical standpoint, this history creates clear collecting objectives. A complete type set of small-size Federal Reserve Notes absolutely requires representation from both sides of the transition: at least one gold-clause note (any denomination, any district) and its post-1933 counterpart. Serious specialists pursue the transition district by district and denomination by denomination, seeking to document exactly how the Bureau of Engraving and Printing implemented the plate changes across its massive printing schedule. Serial number research published by groups such as the Society of Paper Money Collectors has helped narrow down which print runs correspond to which obligation text, giving collectors a framework for attributing transitional pieces.

Conclusion: Paper Money as Living Legislative History

Few pieces of legislation have left as direct and readable a mark on physical currency as the Emergency Banking Relief Act of 1933. Every Federal Reserve Note in your wallet today is a descendant of that eight-day legislative sprint in March 1933. The gold-clause notes that preceded it are tangible relics of a monetary world that ceased to exist in the space of a single congressional session. For the currency collector, that history is not abstract; it is printed, engraved, and sealed in paper and ink, waiting to be read by anyone who knows where to look.