📷 Image source: eBay. Images are selected by AI to represent the article topic and may not depict the exact note(s) described.

Imagine watching your bank lock its doors on a Tuesday morning, not because it was insolvent, but simply because it had run out of cash. That is precisely what happened to thousands of Americans in October and November of 1907, when a speculative scheme gone wrong triggered a cascading panic that froze credit markets from New York to San Francisco. No lender of last resort existed. No central bank stood ready to inject liquidity. The United States government was, in the words of contemporary observers, a financial giant with a glass jaw. The notes, certificates, and scrip that emerged from that chaos tell a story that every serious collector of US paper money needs to know, because the currency system we collect today was born directly from the ashes of 1907.

A Nation Without a Central Bank

To understand the Panic of 1907, you first have to appreciate how genuinely unusual the United States was among industrialized nations at the turn of the twentieth century. Britain had the Bank of England. France had the Banque de France. Germany had the Reichsbank. Each of these institutions could expand credit, act as a lender of last resort, and stabilize their domestic currency in times of stress. The United States had nothing comparable. The First Bank of the United States had been allowed to expire in 1811, and Andrew Jackson had famously destroyed the Second Bank in 1836. In their place stood a patchwork of National Bank Notes, Gold Certificates, Silver Certificates, United States Notes (Greenbacks), and Treasury Notes of 1890, all circulating simultaneously under the National Banking Acts of 1863 and 1864.

This system had one fatal structural flaw: currency elasticity, or rather the total lack of it. National Bank Notes were issued based on a bank’s holdings of US government bonds. When the economy expanded and more currency was needed, banks could not simply issue more notes unless they purchased more government bonds, which were often in short supply or too expensive. Conversely, when a panic hit, banks hoarded reserves, called in loans, and contracted credit at precisely the moment when expansion was needed most. The currency supply was rigidly tied to the bond market rather than to the actual needs of commerce.

The Spark: Heinze, Morse, and the Knickerbocker Trust

The immediate trigger of the 1907 panic was almost farcical in its ambition. F. Augustus Heinze, a copper magnate from Butte, Montana, and his associate Charles W. Morse attempted to corner the stock of United Copper Company in mid-October 1907. The scheme collapsed spectacularly on October 16, sending United Copper shares from roughly $62 down to $15 in a single day. Heinze was connected through a web of trust companies and banks, and when word spread of his failure, depositors began questioning the solvency of every institution he touched.

The Knickerbocker Trust Company of New York, then one of the largest trust companies in the nation with deposits of approximately $65 million, was perceived as connected to the Morse-Heinze network. On October 22, 1907, a run began. Within three hours, Knickerbocker paid out roughly $8 million in cash and then suspended payments entirely. The run immediately spread to the Trust Company of America and the Lincoln Trust Company. Within days, the panic had jumped from New York to regional cities across the country.

National Bank Notes issued during 1907 and 1908 often bear Series 1902 Plain Back or Date Back varieties. Notes from New York and Montana institutions connected to Heinze or Morse that survived this period are historically significant conversation pieces. Look for Charter Numbers in the 3000 to 7000 range from New York City banks, many of which were directly affected by the panic-era liquidity crisis.

J.P. Morgan Plays Central Banker

What saved the American financial system in October 1907 was not the United States government. It was one aging, autocratic private citizen: John Pierpont Morgan, then 70 years old. Morgan essentially convened the entire leadership of New York banking in his personal library at 219 Madison Avenue and refused to let them leave until they agreed to pool their resources and support failing institutions. He organized a $25 million rescue fund for the trust companies, strong-armed the New York Stock Exchange into keeping its doors open with a $25 million loan to brokers, and even coordinated with President Theodore Roosevelt to allow US Steel to acquire the Tennessee Coal and Iron Company in a move designed to prevent the collapse of a major brokerage house.

Treasury Secretary George B. Cortelyou deposited $25 million in federal funds in New York banks to help stabilize reserves. The crisis slowly abated through November, but the damage to confidence had been enormous. The United States had been saved by the personal credit and force of will of one private banker. Every thoughtful observer understood this was no way to run the financial system of a modern industrial democracy.

Clearinghouse Loan Certificates and Emergency Scrip

For currency collectors, the 1907 panic produced some genuinely fascinating and collectible paper. Faced with a shortage of legal tender, the New York Clearing House Association and clearing houses in dozens of other cities issued Clearing House Loan Certificates and, in some cases, actual small-denomination scrip that circulated as currency among citizens. These certificates, technically liabilities of the clearing house rather than legal tender, were issued in denominations ranging from $1 to $10,000 and served as substitutes for cash in bank-to-bank settlements.

Small-denomination scrip appeared in cities including New York, Baltimore, Atlanta, and Portland, Oregon. These notes were printed hastily, often on whatever paper was available, and signed by bank officers. While not legal tender, they were accepted by merchants and citizens desperate for any medium of exchange. Surviving examples of 1907 panic scrip are genuinely scarce collectibles today, representing a direct physical artifact of the crisis. Most examples that surface grade in the Fine to Very Fine range, having actually circulated heavily during those tense weeks.

When researching panic-era emergency scrip, focus on the major auction archives at Heritage Auctions and Stack’s Bowers. The 1907 New York Clearing House certificates in denominations of $5 and $10 occasionally appear and can be authenticated by their distinctive printed signatures and clearing house seals. Always verify with the Society of Paper Money Collectors (SPMC) reference materials before purchasing at premium prices.

The Aldrich-Vreeland Act of 1908: Congress Reacts

The political response to the panic was swift by the standards of the era. On May 30, 1908, Congress passed the Aldrich-Vreeland Act, a temporary measure designed to address the currency elasticity problem while a longer-term solution was developed. The Act did two important things. First, it authorized National Banks to form National Currency Associations that could issue emergency currency backed by commercial paper and state and local bonds rather than solely by US government bonds. Second, it created the National Monetary Commission, chaired by Senator Nelson W. Aldrich of Rhode Island, to study central banking systems around the world and recommend a permanent solution.

The emergency currency provisions of Aldrich-Vreeland would actually be invoked only once, but at a historically significant moment: August 1914, when the outbreak of World War I triggered a financial panic in the United States. Between August and November 1914, approximately $386 million in Aldrich-Vreeland emergency currency was issued and then rapidly retired as the Federal Reserve System came online. These 1914 emergency issues are extremely rare today and represent one of the most significant transitional episodes in US currency history.

Jekyll Island and the Path to the Federal Reserve Act

Senator Aldrich’s National Monetary Commission published dozens of reports between 1908 and 1912. The culmination came in November 1910, when Aldrich convened a secret meeting at the Jekyll Island Club off the coast of Georgia. Attendees included Aldrich himself, Assistant Treasury Secretary A. Piatt Andrew, and leading bankers including Frank Vanderlip of National City Bank, Henry P. Davison of J.P. Morgan and Company, Charles D. Norton of First National Bank of New York, and Paul Warburg of Kuhn, Loeb and Company. Over nine days, this group essentially drafted what became known as the Aldrich Plan, a precursor to the Federal Reserve Act.

The political winds shifted with the 1912 election of Woodrow Wilson, who was skeptical of a plan designed largely by Wall Street bankers. But the core technical framework survived. Congressman Carter Glass of Virginia and Senator Robert Owen of Oklahoma shepherded a revised bill through Congress that decentralized the system into twelve regional Federal Reserve Banks rather than the single central bank Aldrich had envisioned. Wilson signed the Federal Reserve Act on December 23, 1913.

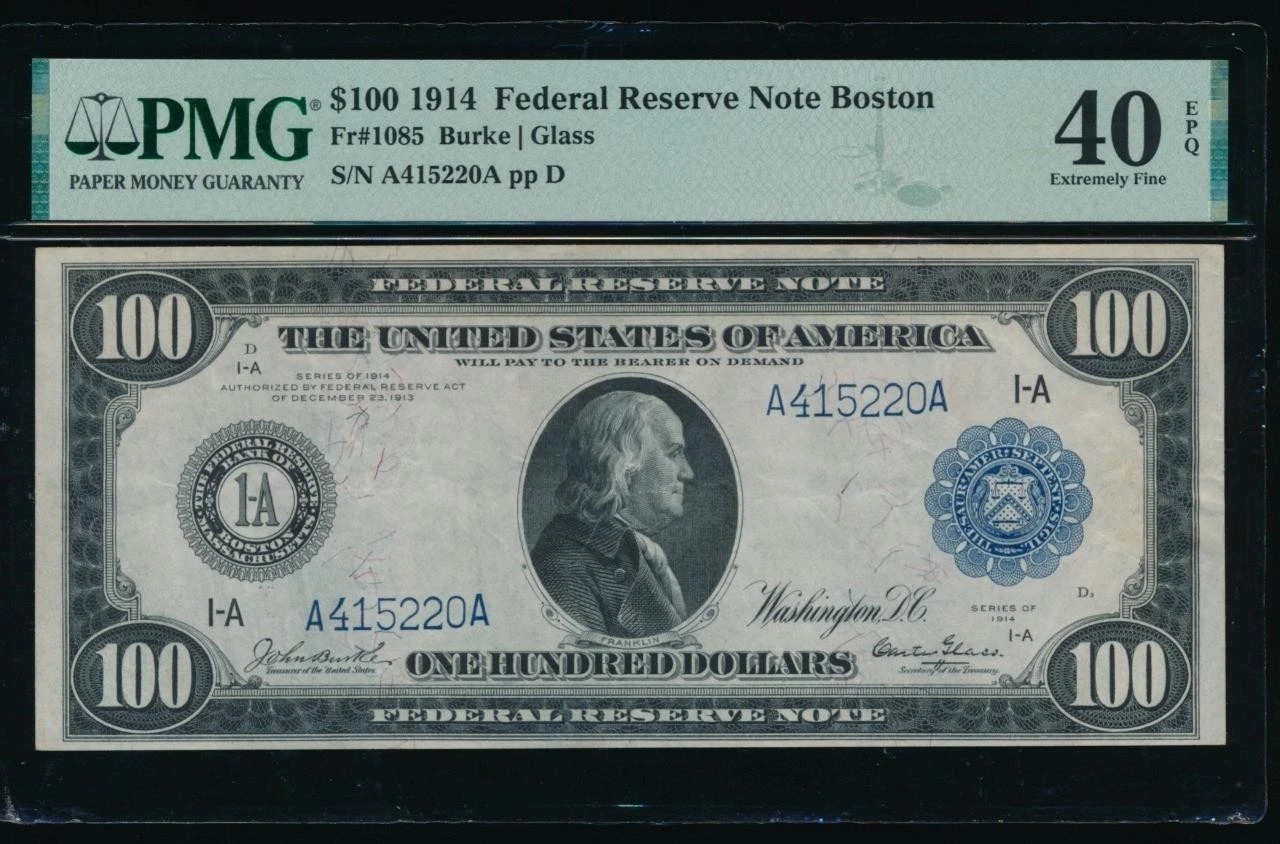

The Series 1914 Federal Reserve Notes: The First FR Currency

The Federal Reserve Banks opened for business on November 16, 1914, and the first Federal Reserve Notes followed in the same series year. The Series 1914 Federal Reserve Notes represent the direct, tangible result of the reforms triggered by the 1907 panic. These notes are among the most collected and historically significant issues in all of US paper money.

Series 1914 Federal Reserve Notes were issued in two distinct varieties that collectors must distinguish. The first issues carried a Red Treasury Seal and Red Serial Numbers, produced in denominations of $5, $10, $20, $50, and $100. These were quickly followed by the far more common Blue Seal and Blue Serial Number variety. The Red Seal 1914 issues are considerably scarcer and command substantial premiums in higher grades. Signatures on the Red Seal notes are exclusively Burke-McAdoo (William S. Burke as Register of the Treasury, William G. McAdoo as Secretary of the Treasury), as McAdoo left office in December 1918. The Blue Seal notes carry five different signature combinations: Burke-McAdoo, Burke-Glass, Burke-Houston, White-Houston, and White-Mellon.

All twelve Federal Reserve Districts issued Series 1914 notes: Boston (A), New York (B), Philadelphia (C), Cleveland (D), Richmond (E), Atlanta (F), Chicago (G), St. Louis (H), Minneapolis (I), Kansas City (J), Dallas (K), and San Francisco (L). District, denomination, and signature combination together determine rarity, and the variation among these factors creates a rich collecting matrix.

For Series 1914 Red Seal Federal Reserve Notes, the $50 and $100 denominations are dramatically scarcer than the $5, $10, and $20 notes. A Red Seal $50 or $100 in VF-25 or better will attract serious competition at any major auction. When buying, insist on PCGS or PMG certified examples, as counterfeits and altered notes (Red Seals created from Blue Seals) do appear in the marketplace.

What the Panic Left Behind in the Currency System

The Federal Reserve Act did not immediately replace all existing currency types. National Bank Notes continued to be issued until 1935. Gold Certificates circulated until 1933. United States Notes (Legal Tender Notes) technically remained in production in token quantities until 1971. But the Federal Reserve Note became, over the following decades, the dominant paper currency of the United States, eventually crowding out every competitor. Every note in your wallet today traces its institutional lineage directly to the panic on the streets of New York in October 1907.

The structural changes went beyond paper money. The Federal Reserve System created a mechanism for expanding and contracting currency based on actual economic need rather than bond holdings. It established check-clearing facilities, created a true lender of last resort, and gave the United States the monetary infrastructure of a mature industrial economy. The irony, not lost on historians, is that a system designed to prevent panics would itself face existential tests in 1929 to 1933, ultimately surviving and evolving into the institution we know today.

| Series / Type | Denomination / District | Approx. Known / Print Run | Rarity |

|---|---|---|---|

| 1914 Red Seal (Burke-McAdoo) | $5, All Districts | Moderate survivors | Scarce |

| 1914 Red Seal (Burke-McAdoo) | $20, All Districts | Fewer survivors | Scarce |

| 1914 Red Seal (Burke-McAdoo) | $50, All Districts | Very few survivors | Rare |

| 1914 Red Seal (Burke-McAdoo) | $100, All Districts | Extremely few survivors | Key Date |

| 1914 Blue Seal (Burke-McAdoo) | $10 and $20, Common Districts | Large print runs | Common |

| 1914 Blue Seal (White-Mellon) | $5, Minneapolis (I) | Low print run | Rare |

| 1914 Blue Seal (Burke-Glass) | $50 and $100, Dallas (K) | Very limited | Rare |

| 1907 Clearing House Scrip | $5 and $10, New York | Fewer than 50 known examples | Key Date |

| 1914 Aldrich-Vreeland Emergency Currency | Various denominations | Extremely rare, most redeemed | Key Date |

| 1914 Blue Seal (White-Houston) | $100, Atlanta (F) | Very limited issuance | Rare |

Collecting the Legacy of 1907

For collectors, the story of the Panic of 1907 opens up several distinct and rewarding avenues. At the highest level, assembling a type set of Series 1914 Federal Reserve Notes across both seal colors and multiple denominations represents a genuine challenge and a historically coherent collection. A complete Red Seal set across all five denominations in problem-free Very Fine or better condition would be a collection of genuine distinction.

At a more accessible level, collectors can focus on the Blue Seal 1914 notes by district, building a twelve-piece set for a single denomination and signature combination. The $10 Blue Seal Burke-McAdoo set by district, for example, offers meaningful rarity variation (Minneapolis and Richmond issues are notably harder to find than New York and Chicago) without requiring the significant capital demanded by the Red Seal high denominations.

Beyond the Federal Reserve Notes themselves, the collector interested in the 1907 story should consider acquiring Series 1902 National Bank Notes from the panic period, perhaps from specific banks documented as participants in clearing house operations during the crisis. The Series 1902 Date Back and Plain Back varieties were the primary circulating notes of the era, and a note from a Manhattan or Brooklyn national bank dated to the 1907 to 1913 window carries real historical resonance.

Conclusion: A Crisis That Rewrote American Currency

The Panic of 1907 lasted only a few weeks in its acute phase, but its consequences reshaped American financial and monetary history for the next century. From the emergency scrip hastily printed in clearing house offices to the elegant engraved Federal Reserve Notes that first appeared in 1914, the paper trail of this crisis is literally collectible. Every collector who holds a Series 1914 Federal Reserve Note is holding the direct physical result of that terrifying October when American banking nearly collapsed and one old man in a Manhattan library held it together with sheer force of will, buying just enough time for Congress to finally build the institution that should have existed all along.