Pick up a Series 1928 Gold Certificate and you are holding a promise. Printed in bold orange-gold ink on the reverse, the note declares it is redeemable in gold coin at the United States Treasury. By the summer of 1933, that promise had been revoked for ordinary American citizens. By August 1971, it was revoked for foreign governments too. These two acts, separated by nearly four decades, fundamentally transformed the nature of American paper money and created some of the most compelling collectibles in the entire field of United States currency.

The Classical Gold Standard and Its Paper Promises

To understand what was lost, collectors need to appreciate what existed. The United States operated on a true domestic gold standard from 1879 onward, following the resumption of specie payments after the Civil War era of Greenbacks. Under this system, paper currency circulated as warehouse receipts for actual gold. Gold Certificates, with their distinctive yellow-orange reverses and “GOLD” printed boldly across their faces, were the most direct expression of this relationship.

The large-size Gold Certificates issued from 1863 through 1922 are extraordinary artifacts. The Series of 1882 $100 Gold Certificate (Friedberg number 1214) bears an engraved portrait of Thomas H. Benton and carries the obligation: “There have been deposited in the Treasury of the United States One Hundred Dollars in Gold Coin payable to the bearer on demand.” These notes circulated primarily among banks and large commercial transactions. The small-size Gold Certificates introduced in 1928, coinciding with the nationwide currency redesign, brought gold-backed notes into everyday pockets for the last time in American history.

Step One: FDR and the Domestic Break of 1933

The banking crisis of early 1933 was severe. Between February and March of that year, bank runs swept the country. When Franklin Roosevelt was inaugurated on March 4, 1933, he immediately declared a national banking holiday under the Emergency Banking Act. But the more consequential act came on April 5, 1933, when Roosevelt signed Executive Order 6102, requiring American citizens to surrender their gold coins, gold bullion, and Gold Certificates to Federal Reserve Banks by May 1, 1933. The penalty for non-compliance was a fine of up to $10,000 and up to ten years imprisonment.

The government paid $20.67 per troy ounce, the statutory price since 1837. Then, in a move that still rankles some economists, Roosevelt signed the Gold Reserve Act on January 30, 1934, which transferred all monetary gold to the U.S. Treasury and revalued it to $35 per troy ounce. In a single stroke, the dollar was devalued by roughly 41 percent relative to gold, and anyone who had surrendered their gold at the old rate received far less than the metal was now officially worth.

When buying Series 1928 Gold Certificates, examine the obligation text carefully. Notes that were officially canceled by the Treasury after the 1933 recall sometimes show punch cancellations or ink stamps. Uncanceled, circulated examples in grades Fine to Very Fine (F-12 to VF-30 on the Sheldon scale) represent genuine survivorship from a period of mandatory government confiscation, which makes condition context especially meaningful.

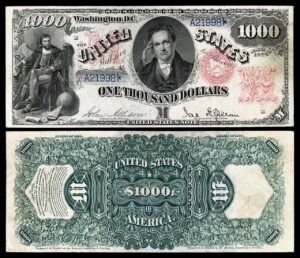

What happened to Gold Certificate printing? The Bureau of Engraving and Printing had produced the small-size Series 1928 Gold Certificates in denominations of $10, $20, $50, $100, $500, $1,000, $5,000, and $10,000. The $10 (Fr. 2400) and $20 (Fr. 2402) notes had the largest production runs and are the most commonly encountered today. The $10 Gold Certificate had a combined print run of approximately 130 million notes across all signature varieties, while the $20 had roughly 66 million printed. Higher denominations saw dramatically lower production. The $500 (Fr. 2407) and $1,000 (Fr. 2408) are genuinely scarce, with total survivors numbering in the hundreds for circulated examples.

After the 1934 Gold Reserve Act, new Gold Certificates were printed exclusively for Federal Reserve Bank internal transfers and were never released to the public. These “post-1934” Gold Certificates (Series 1934, Fr. 2405a through 2408a) are extraordinarily rare in collector hands because private ownership of Gold Certificates was illegal from 1934 until December 31, 1964, when Congress finally lifted the prohibition on collecting them as numismatic items.

Silver Certificates Fill the Void

With Gold Certificates removed from public circulation, Silver Certificates became the dominant redeemable paper currency. Series 1934 and 1935 Silver Certificates promised the bearer “One Dollar in Silver” on demand. These notes are highly collectible today, particularly the Star replacement notes and low-print-run Federal Reserve District issues.

The transition period between 1933 and 1935 produced some transitional currency worth seeking. Series 1934 Federal Reserve Notes bear the signature combination of William A. Julian (Treasurer) and Henry Morgenthau Jr. (Secretary of the Treasury), who replaced William Woodin in January 1934. This Morgenthau era began right as the new monetary regime solidified, and his signature appears on notes through 1945, spanning the entire World War II period.

The Bretton Woods Architecture: Building the Second Promise

The 1933 break was domestic only. Foreign governments and central banks retained the right to exchange U.S. dollars for gold at the Treasury’s official price. When 44 Allied nations convened at the Mount Washington Hotel in Bretton Woods, New Hampshire, in July 1944, they codified this arrangement into a new international monetary architecture. The agreement, signed July 22, 1944, established the U.S. dollar as the world’s reserve currency, with all other currencies pegged to the dollar and the dollar pegged to gold at $35 per troy ounce.

This system worked reasonably well through the 1950s, when the United States held approximately 22,000 tons of gold at Fort Knox and foreign dollar holdings were modest. But the economics of the 1960s eroded the foundation. The Vietnam War, Great Society spending programs, and persistent balance-of-payments deficits flooded the world with dollars. By 1965, foreign central banks held more dollars than the United States held gold to redeem them. France, under Charles de Gaulle’s finance minister Jacques Rueff, began aggressively exchanging dollars for gold in 1965, and others followed. The U.S. gold stockpile fell from a post-war peak of roughly 702 million ounces in 1949 to approximately 289 million ounces by 1971.

Step Two: The Nixon Shock of August 1971

On the evening of Sunday, August 15, 1971, President Richard Nixon interrupted regular television programming to announce three dramatic economic measures. He imposed a 90-day wage and price freeze, placed a 10 percent surcharge on imports, and, most consequentially for monetary history, suspended the convertibility of the dollar into gold. The gold window was closed. Foreign central banks could no longer exchange their dollar reserves for American gold at any price.

Nixon framed the announcement as a temporary measure to protect “the American dollar from the attacks of international money speculators.” It was never temporary. The Smithsonian Agreement of December 18, 1971 attempted to salvage a modified fixed-exchange-rate system, with gold revalued to $38 per ounce. The subsequent Bretton Woods II framework raised the official gold price to $42.22 per ounce in 1973. But the system was crumbling. By March 1973, major currencies had shifted to floating exchange rates, and the dollar’s link to gold was purely nominal. Congress formally severed it by amending the Par Value Modification Act in 1976. Gold’s market price by then was well above $100 per ounce.

Federal Reserve Notes from the late 1960s and early 1970s capture the final years of the Bretton Woods system in tangible form. Series 1969 notes feature the Dorothy Andrews Elston and David M. Kennedy signature combination, while Series 1969-C notes carry the Romana Acosta Bañuelos and John B. Connally signatures. Connally was the Treasury Secretary who sat in the room at Camp David when Nixon made the fateful August 1971 decision. Notes bearing his signature (Fr. 2025-F through 2026-G range and others) are historically resonant collectibles that directly connect to the moment the international gold standard ended.

What Changed on the Notes Themselves

The physical evolution of Federal Reserve Note obligation language tells the story precisely. A Series 1928 Federal Reserve Note reads: “Redeemable in gold on demand at the United States Treasury, or in gold or lawful money at any Federal Reserve Bank.” After the 1933 emergency banking legislation, the obligation was amended. Series 1934 Federal Reserve Notes read: “This note is legal tender for all debts, public and private, and is redeemable in lawful money at the United States Treasury, or at any Federal Reserve Bank.” The word “gold” had been removed from public notes entirely.

By the Series 1963 Federal Reserve Notes, even the redemption language was stripped away. The notes simply read: “This note is legal tender for all debts, public and private.” No promise of exchange into anything of independent value. This linguistic evolution, from gold-backed promise to pure fiat declaration, took exactly thirty years from 1933 to 1963, and the notes themselves document every step.

Collecting the Transition: A Registry of Key Issues

For collectors building a thematic set around the gold standard transition, several specific notes anchor the narrative. The Series 1928 $20 Gold Certificate (Fr. 2402) in Very Fine condition currently trades in the $150 to $250 range, making it accessible. The Series 1934 $100 Gold Certificate (Fr. 2405) issued exclusively for Federal Reserve internal use is a trophy piece, with circulated examples rarely appearing at auction and commanding $5,000 or more. On the Federal Reserve Note side, a complete set of Series 1928 through 1963 $1 notes showing the evolving obligation language can be assembled for under $300 total, representing extraordinary historical value per dollar spent.

| Series / Fr. Number | Denomination and Type | Approx. Print Run | Rarity |

|---|---|---|---|

| 1928 / Fr. 2400 | $10 Gold Certificate | 130,000,000+ | Common |

| 1928 / Fr. 2402 | $20 Gold Certificate | 66,204,000 | Common |

| 1928 / Fr. 2404 | $50 Gold Certificate | 5,964,000 | Scarce |

| 1928 / Fr. 2405 | $100 Gold Certificate | 3,240,000 | Scarce |

| 1928 / Fr. 2407 | $500 Gold Certificate | 420,000 | Rare |

| 1928 / Fr. 2408 | $1,000 Gold Certificate | 288,000 | Rare |

| 1934 / Fr. 2405a | $100 Gold Certificate (Federal Reserve Use) | Classified / Very Low | Key Date |

| 1928 / Fr. 1500 | $1 FRN (Pre-1933 Obligation Language) | 1,800,000,000+ | Common |

| 1934 / Fr. 2051-Ga | $500 FRN (Post-Gold, Chicago Star) | Fewer than 1,000 known | Key Date |

| 1969-C / Various | $1 FRN (Connally Signature, Nixon era) | Varies by district | Common |

The Broader Legacy for Collectors

Understanding the two-step abandonment of the gold standard transforms how a collector reads paper money. A Gold Certificate is not merely an old note with an attractive gold back. It is a surviving artifact from a legal regime that compelled Americans to surrender it under threat of federal prosecution. Federal Reserve Notes from 1933 through 1963 exist in a middle state, partially reformed but still nominally promising “lawful money” redemption. Post-1963 notes are unapologetically fiat, backed by nothing except the authority of the federal government and the productive capacity of the American economy.

None of these characterizations makes one era’s notes more valuable than another in strictly numismatic terms. Rarity, condition, and demand drive prices. But the collector who understands this history brings genuine depth to the hobby. When you hold a Series 1928 $20 Gold Certificate in a PCGS graded holder marked VF-35, you are holding the last generation of American paper money that carried a legally enforceable promise of conversion into a tangible commodity. That is a remarkable thing to hold in your hands, and no amount of monetary policy sophistication should make it feel ordinary.