Walk into any serious currency auction and you will find a category that makes even seasoned collectors pause: National Bank Notes. Hundreds of issuing banks, dozens of states and territories, multiple charter periods, and an almost bewildering variety of vignette combinations make these notes simultaneously the most complex and most rewarding segment of American paper money collecting. At the center of that complexity sits a single piece of legislation: the National Bank Act of June 3, 1864. Revised and strengthened from its 1863 predecessor, the 1864 Act did not just regulate banks. It created a standardized visual language for American currency that lasted more than seven decades and left behind a collecting field unlike any other.

The Problem the 1864 Act Was Solving

To appreciate what the 1864 Act accomplished, you need to understand the chaos it replaced. Before federal banking legislation, each state chartered its own banks under wildly different rules. By 1860, there were more than 1,600 state-chartered banks issuing their own notes, with designs that varied from the artistic to the fraudulent, backed by reserves ranging from solid specie to swamp acreage in the deep South. The so-called “wildcat banking” era produced notes worth anywhere from face value to nearly nothing, and counterfeiters thrived in a landscape where legitimate notes already looked suspicious.

Congress passed the original National Currency Act on February 25, 1863, creating the Office of the Comptroller of the Currency under Hugh McCulloch and establishing a framework for federally chartered banks. But the 1863 law had gaps. Capital requirements were loose, bond-deposit mechanics were imprecise, and the note-design provisions were vague enough to allow considerable variation. The revised and substantially strengthened Act of June 3, 1864 addressed every one of those weaknesses.

Key Provisions That Shaped the Notes Themselves

Several sections of the 1864 Act directly determined what National Bank Notes would look like and who could issue them. Section 7 established minimum capital requirements based on the population of the issuing city. Banks in towns with fewer than 6,000 residents needed at least $50,000 in capital. Those in cities of 6,000 to 50,000 required $100,000. Banks in cities exceeding 50,000 people needed $200,000. These thresholds explain why so many tiny Midwestern towns have entries in the National Bank Note census: a $50,000 capitalization threshold was achievable for a reasonably prosperous farm community in 1870, and those small-town banks produced some of the rarest notes known today.

Section 22 required each nationally chartered bank to deposit US government bonds with the Treasurer of the United States in an amount equal to at least one-third of its paid-in capital, but not less than $30,000. In exchange, the Comptroller would furnish the bank with engraved, printed notes equal to 90 percent of the current market value of those deposited bonds. This bond-collateral mechanism was the engine of standardization: because the notes were printed by the government (initially by the American Bank Note Company and later, from 1875 onward, by the Bureau of Engraving and Printing), the federal government controlled their design entirely.

When attributing a National Bank Note, always begin with the charter number printed on the face. The Comptroller assigned charter numbers sequentially beginning with Charter 1 (First National Bank of Philadelphia, issued 1863). Charter numbers below approximately 2,000 almost always indicate Original Series or Series of 1875 notes from the First Charter Period, which carry strong premiums in any grade.

The Three Charter Periods and Their Visual Signatures

The 1864 Act created an ongoing charter system in which banks applied for 20-year charters and could renew them. This renewal cycle produced the three distinct charter periods that form the backbone of National Bank Note collecting today.

First Charter Period (1863-1882): The Original and 1875 Series

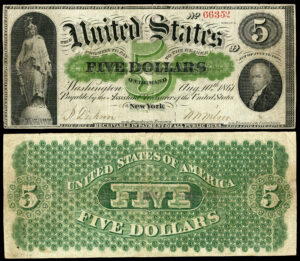

Notes issued under original charters granted between 1863 and 1882 are divided by collectors into the Original Series (printed 1863-1875) and the Series of 1875, which introduced the word “Series” and a date on the face. Both issues share the same large-format design with elaborate border work executed by the American Bank Note Company. The face of a typical $5 First Charter note (Fr. 394-408a) carries the famous “Landing of the Pilgrims” vignette on the left and a portrait of Columbus on the right. The reverse shows the familiar green “Columbus Sighting Land” scene flanked by intricate lathe work. The Treasury seal on these notes is red with scalloped edges.

For collectors, First Charter notes command the highest premiums. A $1 Original Series note (Fr. 380-386) from a large New York or Boston bank in VG condition might sell for $300 to $600, while the same denomination from a rare territorial bank in Very Fine can exceed $10,000. The Series of 1875 $1 (Fr. 387-393) tends to run slightly more available but still attracts strong bids for rare state and territory issues.

Second Charter Period (1882-1902): Brown Backs, Date Backs, and Value Backs

When banks renewed their charters beginning in 1882, they received a new generation of notes in large format but with a redesigned reverse. The three varieties within Second Charter are defined entirely by their reverse treatments, a detail the 1864 Act’s renewal provisions inadvertently made possible by triggering a BEP redesign cycle.

The 1882 Brown Back (Fr. 469-531) is the most visually distinctive, with the charter number printed in large numerals on a brown-tinted reverse. The 1882 Date Back (Fr. 532-577) replaced that design with the printed legend “1882-1908,” referencing the second charter period dates. The 1882 Value Back (Fr. 578-597) substituted the denomination spelled out in words. Collectors prize Value Backs for their relative scarcity: for the $5 denomination, far fewer Value Backs exist than either Brown Backs or Date Backs, a direct consequence of the short window during which they were issued.

The Treasury seal color is one of the fastest ways to narrow down a National Bank Note’s period. Red seals with scalloped rays indicate First Charter. Brown seals indicate Second Charter Brown Backs. Blue seals with small scalloped edges appear on Third Charter notes. However, be cautious: some early Second Charter notes exist with red seals, and these are particularly valuable transitional pieces worth having expertly authenticated.

Third Charter Period (1902-1929): Red Seals, Date Backs, and Plain Backs

The Third Charter Period produced the largest volume of National Bank Notes and, paradoxically, the most common survivors. The 1902 Red Seal (Fr. 613-638), issued only from 1902 until 1908, is the rarest Third Charter variety because its production window was short before the 1902 Date Back replaced it. Date Backs (Fr. 539-612) carry the dates “1902-1908” on the reverse. Plain Backs (Fr. 639-663) dropped the date entirely and were issued from 1908 until the end of large-size National Bank Note production in 1929. The sheer volume of Plain Backs from major city banks means many are genuinely affordable for new collectors, with circulated examples of common banks often available for $75 to $200.

Standardization in Practice: What Every National Bank Note Shares

Despite the enormous variation in issuing banks, dates, and charter periods, the 1864 Act’s standardization provisions ensured that every legitimate National Bank Note shares several features. The Comptroller of the Currency’s signature appears on every note alongside the Treasury Register’s signature, creating a pair of federal certifying officials above and beyond the local bank officers whose signatures also appear. The issuing bank’s charter number appears at least twice on the face of most varieties. The name of the city and state of issue is printed in a dedicated cartouche, creating the geographic collecting dimension that makes this series unique. And the overarching design architecture, controlled by the BEP, ensures that a $10 note from the First National Bank of Podunk, Kansas, and a $10 note from the First National Bank of New York City are recognizably the same type of instrument even as they serve completely different economic communities.

State and territorial collecting is one of the most structured approaches to National Bank Notes. The Standard Catalog of United States Paper Money by Krause and Lemke, combined with Don Kelly’s “National Bank Notes: A Guide with Prices,” gives census data for every reporting bank by state. For rare states like Nevada, New Mexico Territory, and Alaska Territory, even heavily circulated examples can be strong investments because so few notes entered the secondary market to begin with.

The Role of the Comptroller’s Office in Design Control

One of the 1864 Act’s most consequential provisions was concentrating note-design authority entirely in the Comptroller’s office. Individual banks had no say in the artwork, engraving, or color scheme of their notes. They received their allotment from Washington with their name, charter number, and officers’ signature lines already incorporated into the printed design. This was a radical departure from the state-bank era, when individual banks commissioned their own note designs, often resulting in spectacular artistic variety but also easy counterfeiting targets.

The BEP’s control meant that when a design change was made at the federal level, it propagated uniformly across every issuing bank simultaneously. This is why all 1882 Brown Backs share the same reverse regardless of whether they were issued in Maine or Montana. It also means that condition, rarity of issuing bank, and charter period are the three variables that drive value in this market, rather than design uniqueness per se.

Small-Size Nationals: The 1929 Series and the Act’s Final Legacy

The last chapter of National Bank Note production came with the transition to small-size currency in 1929. The Comptroller authorized two types of small-size Nationals: Type 1 (Fr. 1800-1935), which carried the bank’s charter number printed twice in the black serial number arrangement, and Type 2 (Fr. 1800-1935), introduced in 1933, which added a second charter number printed in the brown serial number position. Type 2 notes exist from a significantly smaller number of banks and are substantially rarer across the board. The entire small-size National Bank Note program ended on May 20, 1935, when the last notes were redeemed and the Federal Reserve System completed its takeover of the commercial currency function the 1864 Act had created.

| Series / Type | Denomination and Variety | Approx. Known Examples | Rarity |

|---|---|---|---|

| Original Series (1863-1875) | $1, First Charter, major city bank | Hundreds surviving | Scarce |

| Original Series (1863-1875) | $1, First Charter, territorial issue | Fewer than 30 known per territory | Key Date |

| Series of 1875 | $2, First Charter (Fr. 387-393) | Approx. 150-300 total | Rare |

| 1882 Brown Back | $5, large city issue (Fr. 469-478) | Thousands surviving | Common |

| 1882 Value Back | $5 (Fr. 578-579) | Fewer than 500 known | Rare |

| 1902 Red Seal | $10 (Fr. 613-618) | Scarce across most banks | Scarce |

| 1902 Plain Back | $10, major Federal Reserve city bank | Very large survival population | Common |

| 1929 Type 1 | $20, common state charter | Widely available | Common |

| 1929 Type 2 | Any denomination, single-bank issuer | Often fewer than 10 known | Key Date |

| 1929 Type 1 or 2 | Any denomination, Alaska or Hawaii territory | Extremely few per bank | Key Date |

Why This Matters for Collectors Today

The National Bank Act of 1864 created a collecting field with built-in structure. Because every note carries a charter number and issuing city, the census of survivors can be systematically studied and tracked. Organizations like the Society of Paper Money Collectors maintain specialized research groups for National Bank Notes, and the work of researchers like Andrew Shiva (whose online National Bank Note census database covers thousands of banks) gives today’s collector tools that would have seemed miraculous to the early specialists of the 1950s and 1960s.

For new collectors, the advice is straightforward: start with Third Charter Plain Backs from your home state or a geographic area that interests you personally. These notes are affordable, genuinely historical, and immediately legible as documents of local economic life. As your knowledge grows, you will naturally begin to notice the signature combinations, the seal varieties, and the design subtleties that the 1864 Act’s standardization both enabled and constrained. That is when the collecting really begins.

The 1864 Act was never written with collectors in mind. It was written to prevent financial panics, to fund the Civil War, and to build a coherent national banking system from the ruins of wildcat chaos. But in accomplishing those utilitarian goals, it inadvertently created the most historically rich and geographically diverse series of notes in American numismatics, and collectors have been grateful ever since.