📷 Image source: U.S. Currency Education Program (uscurrency.gov). Images are selected by AI to represent the article topic and may not depict the exact note(s) described.

Few episodes in American financial history carry the drama, consequence, and sheer personality of Andrew Jackson’s war against the Second Bank of the United States. Between 1832 and 1836, one stubborn Tennessee frontiersman-turned-president dismantled the closest thing the young republic had to a central bank, and the paper money landscape of the 1830s bears the scars and the splendor of that decision. For collectors who hold antebellum banknotes in their hands today, those worn, ornately engraved notes are not merely currency. They are artifacts of a constitutional showdown, a currency meltdown, and an era of breathtaking monetary experimentation.

The Second Bank: A Brief Portrait of the Enemy

The Second Bank of the United States was chartered in April 1816, rising from the fiscal wreckage of the War of 1812. Headquartered in Philadelphia in a stately Greek Revival building that still stands today, it operated with $35 million in capitalization, one-fifth of which was subscribed by the federal government. Its mandate was ambitious: provide a uniform national currency, regulate the lending of state-chartered banks, and act as fiscal agent for the Treasury.

By the late 1820s, under the capable presidency of Nicholas Biddle, the BUS was functioning exactly as designed. Biddle used the bank’s enormous reserves of state banknotes, accumulated as deposits from across the country, as a disciplinary tool. When a state bank issued notes too aggressively, the BUS would present those notes for redemption in specie, forcing the offending bank to contract its lending. The system was imperfect but effective. The currency of the early 1830s, while far from uniform in appearance, was reasonably well-regulated in value.

Jackson despised all of it. His antipathy was partly philosophical, rooted in a hard-money Jeffersonian suspicion of banks, paper currency, and concentrated financial power. It was partly personal: he had suffered losses in land speculation financed by unreliable paper money decades earlier. And it was partly political: the BUS was, in Jackson’s view, a monster that served Eastern moneyed elites at the expense of Western farmers and working men. When Biddle and his congressional allies, led by Henry Clay, forced a recharter bill through Congress in July 1832, four years before the existing charter expired, they handed Jackson the political weapon he had been waiting for.

The Veto and Its Immediate Monetary Consequences

Jackson’s veto message of July 10, 1832 is one of the most remarkable documents in American political history. It reads less like a legal brief than a populist broadside, attacking the bank as unconstitutional, un-American, and a threat to democracy. Congress failed to override it, and the BUS was effectively sentenced to death. Its charter would expire in 1836 and would not be renewed.

The monetary consequences began almost immediately. Jackson’s Treasury Secretary, Roger Taney, began removing federal deposits from the BUS in October 1833, redistributing them to a rotating cast of state-chartered banks that critics quickly labeled “pet banks.” The BUS, its lifeblood draining away, contracted credit sharply throughout 1833 and into 1834, triggering a brief but painful recession. Biddle intended the contraction as a demonstration of the bank’s necessity, a strategy that backfired politically even as it caused genuine economic suffering.

Notes issued by the Second Bank of the United States itself are among the most historically significant American banknotes you can own. Look for branch drafts and notes from BUS branches in cities like Cincinnati, Louisville, and New Orleans. Even heavily circulated examples carry enormous historical weight. Authenticate carefully: counterfeits of popular BUS notes existed in period and reproductions exist today.

The Wildcat Era: Paper Money Explodes

Once the disciplinary hand of the BUS was removed, state banks multiplied with astonishing speed. From roughly 330 state-chartered banks in 1830, the number swelled to approximately 788 by 1837. In states with loose chartering laws, particularly in the South and West, banks sprang up in locations so remote that critics joked a noteholder would need to hike through wilderness to find the bank for redemption, which is precisely where the term “wildcat banking” may have originated, though its etymology remains debated.

Each of these banks issued its own paper currency, redeemable in specie on demand but often backed by little more than optimism and frontier real estate. The variety was staggering. A merchant in Cincinnati in 1835 might handle notes from dozens of different institutions on a single business day, each with its own engraved vignettes, denomination typography, and redemption reliability. Counterfeit detectors, publications that listed known fraudulent issues and described genuine notes in minute detail, became essential business tools. Publications like “Bicknell’s Counterfeit Detector” thrived precisely because the currency landscape had become ungovernable.

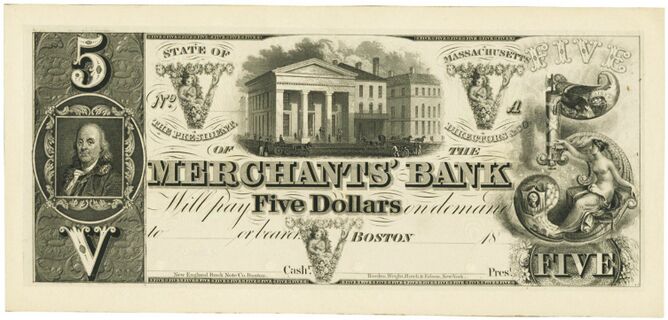

For today’s collector, this explosion of note-issuing activity produced an extraordinary diversity of survivable material. Obsolete banknotes from the 1830s represent some of the finest examples of early American engraving. Firms like Rawdon, Wright, Hatch and Company, and the New England Bank Note Company produced vignettes of breathtaking quality: idealized agricultural scenes, allegorical female figures representing Liberty and Commerce, portraits of founding fathers, and wildlife imagery that reflected regional pride. A $5 note from the Bank of Tennessee dated 1838 or a $3 note from a Michigan territorial bank circa 1835 is as much a piece of printmaking history as it is a monetary document.

When collecting 1830s obsolete banknotes, pay close attention to the engraving firm imprint, usually found at the bottom of the note. Notes engraved by Rawdon, Wright, Hatch and Company or Draper, Toppan, Longacre and Company command premiums among serious collectors because of the artistry involved. The imprint is also a key authentication point, as period counterfeiters rarely replicated engraver credits with full accuracy.

Speculative Frenzy and the Specie Circular

By 1835 and into 1836, the removal of BUS oversight had combined with cheap state bank credit to fuel a speculative land boom of historic proportions. Federal land sales, which had averaged roughly $2.3 million per year in the early 1830s, exploded to $24.9 million in 1836. Much of that land was purchased with the inflated paper notes of pet banks and frontier institutions, many of which had issued far more currency than their specie reserves could support.

Jackson, alarmed by the bubble his own policies had helped inflate, issued the Specie Circular on August 15, 1836. The executive order required payment for government lands to be made in gold or silver coin, effectively invalidating the paper currency that had been fueling the boom. The effect was swift and brutal. Demand for specie spiked. State banks, unable to meet redemption demands, began suspending specie payments in May 1837, triggering the Panic of 1837, one of the worst depressions in American history to that point.

The banknotes circulating in May 1837 became, overnight, instruments of uncertain value. Some banks resumed specie payments within a year. Others never did, closing their doors and leaving noteholders with worthless paper. It is precisely this mortality that makes surviving notes from failed 1830s banks genuinely rare and historically poignant. A note from the Bank of Brussels, Michigan, dated 1835 and never redeemed, tells a story of broken promises and frontier financial wreckage that no textbook can fully capture.

Notes from banks that failed during or shortly after the Panic of 1837 often survive in higher grades because they circulated only briefly before the bank closed. If you encounter a crisp, well-preserved note from a short-lived Michigan, Indiana, or Illinois bank of the mid-1830s, do not assume it is a reprint. Verify with reference works like Haxby’s “Standard Catalog of United States Obsolete Bank Notes” to determine whether the bank’s history supports a short circulation period.

Treasury Notes: The Federal Government’s Awkward Answer

With the BUS gone and the banking system in chaos, the federal government found itself needing a way to manage its own finances without a central bank. The answer was Treasury Notes, interest-bearing government obligations that could circulate as a quasi-currency. Congress authorized Treasury Note issues in 1837, 1838, 1840, 1841, and 1842, in denominations ranging from $50 to $1,000, with interest rates varying by issue from 1 mill per day to 6 percent per annum.

These notes were not legal tender in the strict sense, but they were receivable for government dues and widely accepted in commerce. They represent a crucial bridge between the antebellum state bank era and the later greenback currency of the Civil War. For collectors, genuine 1837 to 1842 Treasury Notes in any grade are significant finds. They were issued in small quantities relative to state bank paper, and many were redeemed and destroyed. A Treasury Note from the Act of October 12, 1837, bearing the signatures of Treasury officials of the Van Buren administration, is a direct artifact of the governmental scrambling that followed Jackson’s Bank War.

| Note Type / Issue | Denomination or Variety | Approx. Surviving Examples | Rarity |

|---|---|---|---|

| BUS Branch Note, Philadelphia, 1832 | $5, Biddle-era issue | Fewer than 50 known | Key Date |

| BUS Branch Draft, New Orleans, 1835 | $100 sight draft | Fewer than 20 known | Key Date |

| US Treasury Note, Act of Oct. 12, 1837 | $50 to $1,000 | Under 100 total across denominations | Rare |

| Bank of Michigan Territory, 1835 | $3 and $5 denominations | Estimated 150 to 300 | Rare |

| Bank of Brussels (Michigan), 1835 | $1, $2, $3 | Estimated 200 to 400 | Scarce |

| Bank of Tennessee State Notes, 1838 | $5, $10 issues | Several hundred known | Scarce |

| Pet Bank Notes (selected Ohio issues), 1836 | $1 to $20 | Moderate survivors | Common |

| New England Merchant Bank Notes, 1834 to 1837 | $1 to $5 | Widely surviving | Common |

What the Bank War Means for Collectors Today

Jackson’s Bank War did not just reshape monetary policy. It created the conditions for the most diverse, visually extraordinary, and historically layered chapter in American paper money history. The 1830s produced currency from more individual issuers than any other decade before or since. Collectors who specialize in this era are essentially building a three-dimensional map of Jacksonian America: its geographic expansion, its speculative appetite, its artistic ambitions, and its catastrophic financial overreach.

The market for quality 1830s obsolete notes has strengthened considerably in recent years. A Choice Uncirculated example from a failed wildcat bank, particularly one with strong vignette color and an interesting geographic or political connection, can command four figures at specialized auction. PCGS Currency and PMG both grade obsolete notes, and a graded, problem-free example from this era carries a meaningful premium over raw equivalents.

When you hold a $5 note from a now-vanished Indiana bank, engraved with scenes of frontier agriculture and signed by men whose names appear in no history book, you are holding the direct consequence of a political war waged nearly two centuries ago. Andrew Jackson wanted to destroy a bank. He succeeded, and in the wreckage, American paper money bloomed into a thousand varieties. For collectors, that is a legacy well worth preserving.